North America Home Automation Systems Market Size

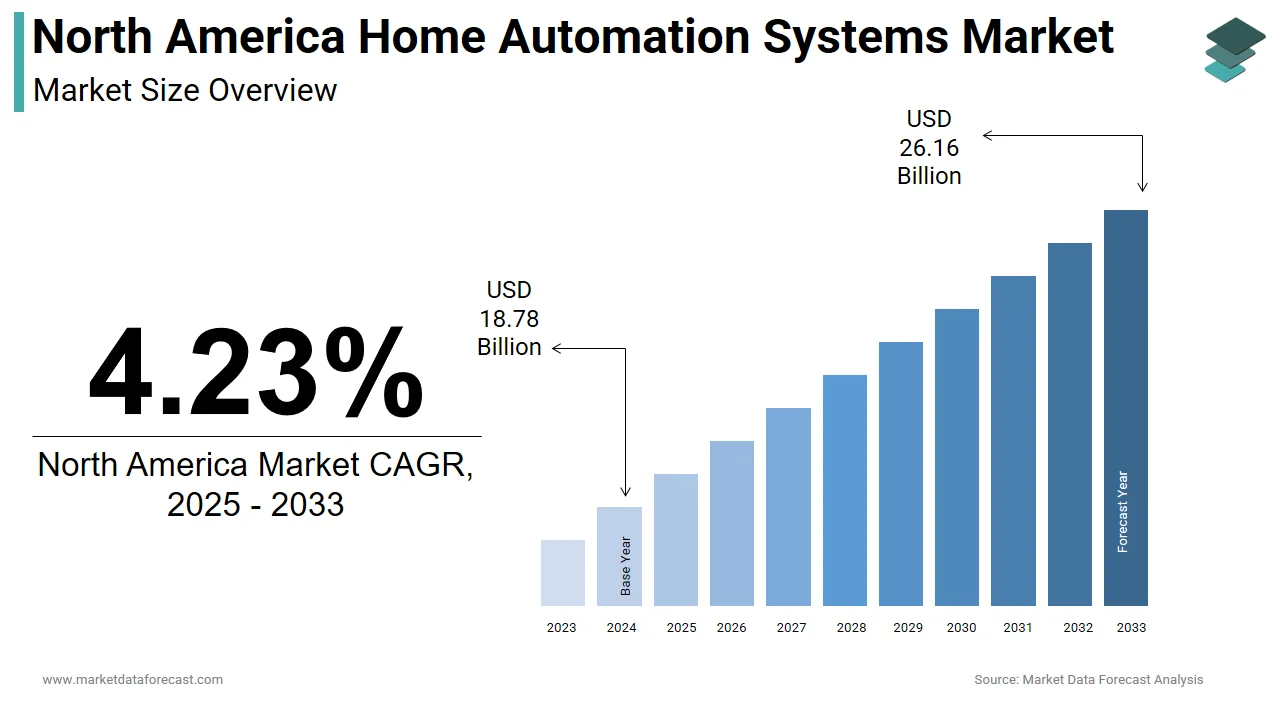

The North America home automation systems market was valued at USD 18.02 billion in 2024, is estimated to reach USD 18.78 billion in 2025, and is projected to reach USD 26.16 billion by 2033, growing at a CAGR of 4.23% from 2025 to 2033.

The home automation system is a network of interconnected devices and intelligent technologies designed to remotely monitor, control, and optimize residential environments, including lighting, climate, security, and entertainment systems. This ecosystem leverages Internet of Things (IoT) infrastructure, cloud computing, and artificial intelligence to enhance convenience, energy efficiency, and occupant safety. As of 2023, over 78% of households in the United States had broadband internet subscriptions, as the Federal Communications Commission reported, facilitating real-time communication between smart devices. Additionally, the U.S. Census Bureau indicates that single-family housing completions reached approximately 940,000 units in 2023, reflecting sustained residential construction activity that increasingly incorporates smart technologies at the design stage. Canada has also witnessed growing adoption, with Natural Resources Canada noting that over 40% of new residential constructions in major provinces now include pre-wired automation infrastructure.

MARKET DRIVERS

Growing Consumer Emphasis on Energy Efficiency and Sustainability

The increasing consumer prioritization of energy efficiency and sustainable living is accelerating the growth of the North America home automation systems market. Homeowners actively seek solutions that reduce utility consumption and carbon footprints, prompting widespread integration of smart thermostats, intelligent lighting, and energy management systems. According to the U.S. Energy Information Administration, residential electricity consumption in the United States accounted for approximately 38% of total end-use energy expenditures in 2023, creating a compelling financial incentive for optimization. Smart thermostats, such as those offered by Nest and Ecobee, have demonstrated the ability to reduce heating and cooling costs by up to 23%, as validated by studies conducted by the American Council for an Energy-Efficient Economy.

Proliferation of 5G Networks and High-Speed Connectivity Infrastructure

The rapid deployment of 5G networks and advancements in broadband infrastructure are fuelling the growth of the North America home automation systems market. Unlike previous generations of wireless technology, 5G offers ultra-low latency, high bandwidth, and enhanced device density support, enabling seamless real-time communication among dozens of interconnected smart devices within a single residence. This robust connectivity landscape allows for instantaneous command execution for applications such as voice-activated controls, remote surveillance, and AI-driven predictive automation. For instance, AT&T reported in 2023 that its 5G-enabled smart home trials achieved response times under 10 milliseconds, significantly improving user experience. Moreover, the Federal Communications Commission notes that over 100 million U.S. households now have access to gigabit-speed internet, fostering the adoption of bandwidth-intensive automation platforms like whole-home video analytics and cloud-based AI assistants. This infrastructure evolution is not only enhancing system reliability but also enabling the emergence of edge computing within residential environments, where data processing occurs locally rather than in distant servers by reducing latency and improving privacy.

MARKET RESTRAINTS

High Upfront Installation and Integration Costs

The substantial initial investment required for equipment procurement and professional installation is quietly hindering the growth of the North America home automation systems market. While operational savings are well-documented, the upfront cost of a fully integrated smart home system can exceed $5,000 for mid-tier configurations, with premium setups surpassing $15,000, according to data from the Consumer Technology Association in 2023. This includes expenses related to smart hubs, sensors, security cameras, climate controls, and labor-intensive wiring for legacy homes. A survey conducted by the National Association of Home Builders revealed that 62% of homeowners cite cost as the primary barrier to adopting advanced automation technologies. Additionally, interoperability challenges between brands increase complexity and cost, requiring third-party integration platforms or custom programming. The lack of standardized protocols across manufacturers means that consumers may face vendor lock-in or require additional middleware, driving up total ownership costs. In Canada, the Canadian Home Builders’ Association notes that only 28% of existing homeowners opt for comprehensive automation retrofits due to financial constraints, despite interest in energy savings.

Cybersecurity Vulnerabilities and Data Privacy Concerns

The escalating risk of cybersecurity breaches and data privacy violations is also slowing down the growth of the North America home automation systems market. According to the Federal Trade Commission, complaints related to smart home device hacking increased by 68% between 2021 and 2023, with over 27,000 incidents reported in 2023 alone. Many entry-level smart devices lack robust encryption, regular firmware updates, or multi-factor authentication, which makes them susceptible to unauthorized access. A 2023 report by the Cybersecurity and Infrastructure Security Agency (CISA) identified that 60% of consumer-grade smart home devices operate on outdated software frameworks with known security flaws. Furthermore, the Internet Society’s Global Internet Report highlights that 73% of smart home data transmissions in North America occur over unsecured Wi-Fi networks, increasing the risk of interception.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Predictive Analytics

The integration of artificial intelligence (AI) and predictive analytics to deliver personalized, adaptive living environments is positively impacting the growth of the North America home automation systems market. Modern AI-powered platforms can learn user behavior, anticipate needs, and autonomously adjust settings for lighting, temperature, and security based on historical patterns and contextual inputs. As per the Stanford Institute for Human-Centered Artificial Intelligence, AI adoption in consumer IoT devices grew by 52% in 2023, with smart home applications representing the fastest-growing segment. Google’s AI subsidiary DeepMind reported that its adaptive learning algorithms reduced HVAC energy consumption by 18% in trial deployments by predicting occupancy patterns with 92% accuracy.

Expansion of Smart Building Codes and Municipal Incentive Programs

The growing implementation of smart building codes and municipal-level incentive programs aimed at modernizing residential infrastructure is also to elevate the growth of the North America home automation systems market. Cities across the United States and Canada are adopting regulatory frameworks that mandate or incentivize the inclusion of intelligent systems in new constructions and major renovations. For example, the 2024 edition of the International Energy Conservation Code (IECC) requires demand-responsive HVAC controls and lighting automation in all new residential buildings exceeding 3,000 square feet, a provision expected to influence over 300,000 annual housing units, as estimated by the International Code Council. In California, Title 24 regulations now necessitate solar-readiness and smart meter integration in all new homes, accelerating automation adoption. Additionally, utility companies are partnering with automation vendors; Pacific Gas & Electric’s Smart Homes Program distributed over 120,000 free smart thermostats in 2023 to qualifying customers.

MARKET CHALLENGES

Interoperability Fragmentation Across Ecosystems

The lack of universal interoperability among devices from different manufacturers which is likely to hamper the growth of the North America home automation systems market. According to the Institute of Electrical and Electronics Engineers, only 38% of smart home devices sold in North America in 2023 were Matter-certified, leaving a majority incompatible across platforms. This fragmentation forces consumers to commit to single vendors, limiting flexibility and increasing long-term costs. A 2023 study by Parks Associates found that 44% of smart home owners experienced difficulties connecting devices from different brands, with 29% abandoning automation projects due to integration issues. Moreover, firmware inconsistencies and varying update cycles exacerbate incompatibility. The National Institute of Standards and Technology emphasizes that the absence of a unified communication protocol increases cybersecurity risks and complicates troubleshooting.

Workforce Shortages in Smart Home Installation and Technical Support

The acute shortage of skilled professionals capable of installing, configuring, and maintaining complex smart home systems is inhibiting the growth of the North America home automation systems market. According to the U.S. Bureau of Labor Statistics, the number of certified home technology professionals (CHTPs) increased by only 12% between 2021 and 2023, while smart home installations rose by 39% in the same period. The Custom Electronic Design & Installation Association (CEDIA) reports a deficit of over 15,000 qualified installers across North America as of 2023, leading to extended service wait times and project delays. This shortage is particularly acute in rural and suburban areas, where 68% of consumers face wait times exceeding four weeks for professional installation, as per a 2023 survey by Statista. Moreover, rapid technological evolution necessitates continuous upskilling, yet only 31% of technicians participate in annual certification programs, according to the Electronics Technicians Association.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product, Protocol, Residence Type, System Type, Installation Type, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

United States, Canada, Mexico, Rest of North America |

|

Market Leaders Profiled |

Johnson Controls Inc. (Ireland), Honeywell International Inc. (US), Schneider Electric (France), Siemens (Germany), Legrand (France), Apple Inc. (US), Resideo Technologies Inc. (US), Robert Bosch (Germany), ABB (Switzerland), Loxone Electronics GmbH (Austria), Vivint, Inc. (US), Nice S.p.A. (Italy), eufy (UK), The Domotics (India), OKOS (US)., and Others. |

SEGMENTAL ANALYSIS

By Product Insights

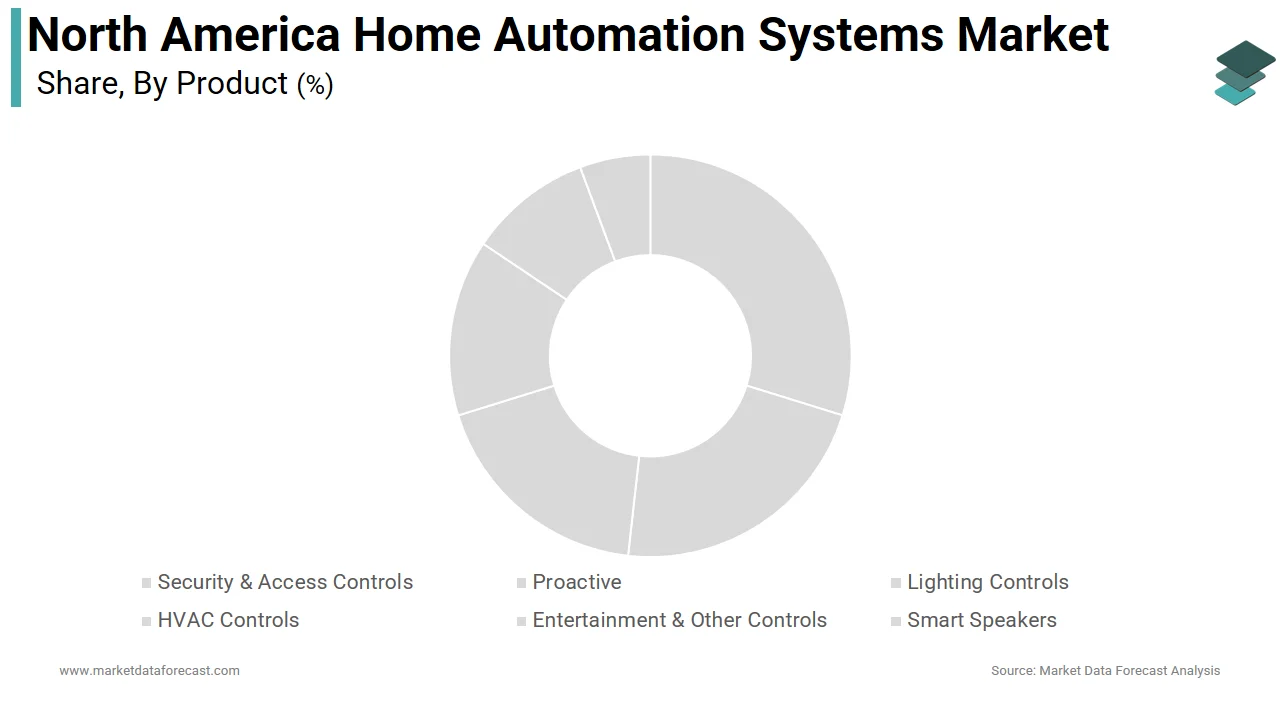

The security & access controls segment held 28.3% of the North America home automation systems market share in 2024, with the escalating incidence of property-related crime and the public’s heightened awareness of preventive security solutions. As per the Federal Bureau of Investigation’s 2023 Crime in the United States report, there were over 1.8 million reported burglaries across the U.S., with residential properties accounting for 68% of incidents, fueling demand for real-time monitoring and deterrent technologies. Additionally, the integration of AI-powered analytics into security devices has significantly enhanced their functionality.

The Proactive Automation Systems segment is likely to expand with an expected CAGR of 18.7% during the forecast period, with the advancement in edge computing capabilities by enabling on-device data processing without cloud dependency. According to the Institute of Electrical and Electronics Engineers, edge AI chip shipments in smart home devices reached 89 million units in North America in 2023, a 63% increase from the previous year. These chips allow systems to learn occupancy patterns, weather fluctuations, and energy pricing trends to optimize HVAC, lighting, and appliance usage in real time. For instance, Google Nest’s Proactive Thermostat mode, introduced in 2023, reduced average heating costs by 21% by predicting user return times with 89% accuracy, as verified by the American Council for an Energy-Efficient Economy. Additionally, integration with utility demand-response programs has amplified adoption. Pacific Gas & Electric reported that over 310,000 customers enrolled in its automated energy-saving programs in 2023, where homes dynamically adjusted energy use during peak pricing hours.

COUNTRY LEVEL ANALYSIS

The United States Home Automation Systems Market Insights

The United States was the top performer in the North America home automation systems market by capturing 76.4% share in 2024 with its advanced digital infrastructure, high disposable income, and a deeply entrenched culture of technological adoption. Moreover, the proliferation of tech-integrated new constructions is accelerating market expansion, with the National Association of Home Builders confirming that 68% of newly built single-family homes in 2023 included at least one smart system, primarily security or climate control. Federal and state-level incentives further stimulate adoption, with the Inflation Reduction Act allocating $8.8 billion for home energy rebates linked to smart thermostat and HVAC upgrades. Major technology firms such as Amazon, Google, and Apple continue to drive innovation and consumer engagement through ecosystem integration, while retail penetration via platforms like Best Buy and Home Depot ensures widespread accessibility. The convergence of regulatory support, private-sector investment, and consumer readiness positions the U.S. not only as the largest market but as the primary innovation engine shaping the future of home automation across North America.

Canada Home Automation Systems Market Insights

Canada was positioned second in the North America home automation systems market with 16.2% of share in 2024, with the steady urbanization, strong government support for energy efficiency, and increasing consumer interest in sustainable living. Additionally, Canada’s National Energy Code for Buildings now encourages, and in some provinces mandates, the integration of demand-responsive systems in multi-unit residential buildings. Internet penetration is another enabling factor, with 96.5% of households having access to broadband services, as reported by the Canadian Radio-television and Telecommunications Commission. Major telecom providers like Rogers and Bell have launched bundled smart home packages, which are contributing to a 43% year-over-year increase in subscription-based automation services in 2023.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America home automation systems market profiled in the report are Johnson Controls Inc. (Ireland), Honeywell International Inc. (US), Schneider Electric (France), Siemens (Germany), Legrand (France), Apple Inc. (US), Resideo Technologies Inc. (US), Robert Bosch (Germany), ABB (Switzerland), Loxone Electronics GmbH (Austria), Vivint, Inc. (US), Nice S.p.A. (Italy), eufy (UK), The Domotics (India), OKOS (US)., and Others.

TOP LEADING PLAYERS IN THE MARKET

Google LLC

Google has emerged as a pivotal force in the North America home automation systems market through its deeply integrated ecosystem of AI-driven devices and voice-enabled platforms. Leveraging its Nest product line, the company offers intelligent thermostats, security cameras, and smart displays that seamlessly interact with its broader suite of services. Google’s strength lies in its ability to unify hardware, software, and cloud intelligence, creating a cohesive user experience that emphasizes predictive automation and energy efficiency.

Amazon.com, Inc.

Amazon has established a dominant presence in the North America home automation systems market through its Alexa-powered ecosystem and extensive portfolio of Echo devices. The company’s strategy revolves around making voice-controlled automation accessible, intuitive, and deeply embedded in daily routines. Its focus on seamless integration, cloud-based intelligence, and retail-driven distribution through Amazon.com enables rapid consumer adoption. The company also invests heavily in security and privacy features to build trust in its ecosystem. Amazon’s ability to combine hardware innovation with a vast digital marketplace allows it to influence both consumer behavior and industry standards by making it a key enabler of smart home proliferation across diverse household types.

Apple Inc.

Apple plays a distinctive role in the North America home automation systems market by prioritizing privacy, design, and ecosystem cohesion. Through its HomeKit platform and integration with Siri, the company enables users to control compatible devices using iPhones, iPads, and HomePods with a strong emphasis on end-to-end encryption and data security. Apple’s approach appeals to premium consumers who value seamless interoperability within a closed, high-quality ecosystem. The company’s recent support for the Matter standard reflects a strategic shift toward broader compatibility without compromising its core principles. Its influence extends beyond hardware, shaping industry expectations for user experience, security protocols, and minimalist design in the automation space.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading companies is ecosystem integration, where firms create closed-loop environments that connect hardware, software, and cloud services to deliver a seamless user experience. Another key approach is strategic standardization, particularly through participation in universal protocols like Matter, which enables cross-brand compatibility and reduces consumer hesitation due to interoperability concerns. This collaborative move helps unify a fragmented market and accelerates mainstream adoption.

COMPETITIVE LANDSCAPE

The competitive landscape of the North America home automation systems market is characterized by a dynamic interplay between technology giants, specialized hardware manufacturers, and emerging innovators. Dominance is largely held by multinational corporations with extensive digital ecosystems, enabling them to integrate automation into broader consumer technology experiences. However, the market remains fragmented across device categories and communication protocols, creating space for niche companies to thrive by focusing on specific applications such as security, energy management, or accessibility. Competition is not solely based on product features but increasingly on ecosystem coherence, data privacy standards, and ease of integration. Companies are under constant pressure to innovate while ensuring compatibility across platforms, especially with the rise of universal standards. Partnerships between tech firms, telecom providers, and homebuilders are reshaping market dynamics, enabling embedded automation in new constructions.

RECENT MARKET DEVELOPMENTS

- In June 2023, Google launched its next-generation Nest Hub with enhanced facial recognition and sleep-tracking capabilities, which is integrating it deeper into its home health and wellness automation strategy. This advancement reinforced Google’s focus on personalized, AI-driven home experiences.

- In September 2023, Amazon introduced a new Matter-enabled Echo Dot with temperature and humidity sensors by expanding its device intelligence and reinforcing its dominance in interoperable smart home ecosystems.

- In January 2024, Apple announced native Matter support across its HomeKit-enabled devices, allowing seamless connectivity with non-Apple smart products, which is marking a strategic shift toward broader compatibility without compromising privacy.

- In March 2024, Samsung SmartThings partnered with ADT to integrate professional security monitoring with consumer-controlled automation by bridging the gap between DIY and enterprise-grade home protection.

- In May 2024, Lutron Electronics expanded its Caséta wireless system to include adaptive lighting that syncs with circadian rhythms by enhancing its position in the premium residential automation segment.

MARKET SEGMENTATION

This North America home automation systems market research report is segmented and sub-segmented into the following categories.

By Product

- Security & Access Controls

- Proactive

- Lighting Controls

- HVAC Controls

- Entertainment & Other Controls

- Smart Speakers

By Protocol

By Residence Type

- Single-Family

- Multi-Family

By System Type

By Installation Type

- New Installation

- Retrofit Installation

By Country

- United States

- Canada

- Mexico

- Rest of North America